Photo via Colin DiCarlo

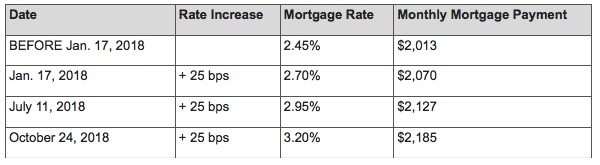

For the fifth time since the Summer of 2017, the Bank of Canada raised its main interest rate. If millennials thought they were already screwed, this latest move—which is likely to be followed by three more hikes next year—can be downright discouraging. Today’s increase to 1.75 percent from 1.5 percent, combined with condo prices that continue to march higher in Vancouver and Toronto, and a higher bar to qualify for a mortgage, have made affording a home even tougher, and millennials are disproportionately affected.“We’re basically pricing out many young Canadians,” says CIBC World Markets Deputy Chief Economist Benjamin Tal who says this phenomenon is already being seen in the numbers. Mortgage borrowing has dropped to its lowest level since 2014. “You’d have to be in a recession to see mortgage activity slowing so quickly. So it is a big big story.”It’s a story 26-year-old Colin DiCarlo knows too well. He began shopping for his first home about 18 months ago, right before the central bank started raising rates. “Even though I’ve gotten a couple of promotions and my career seems to be going in a great direction, I still feel further away now than I did a year ago from being able to get into the market.”DiCarlo is a manager for Red Bull events, based in Toronto. He says he checks real estate listings daily and he’s targeting a $500,000 (with 20 percent earmarked for a down payment) range for his first home which will likely be a one-bedroom condo with minimal square footage. Despite his steadily increasing earnings, what he has to set aside for his entry point into the housing market has ballooned. “It feels overinflated to me. I don’t know how anybody in my generation can get in it in a realistic sense,” says the Halifax transplant. In addition to the five rate hikes (three total this year), condo prices in Toronto continue to outperform and those cater to a lot of millennial buyers. So while prospective buyers like DiCarlo have been saving, prices have risen. He also has to save more to qualify for a mortgage because of new federal rules, known as B20, imposed by Canada’s top bank regulator. As of January 1, home ownership hopefuls like DiCarlo must prove they can service a mortgage based on one of two things (depending on which is higher): the Bank of Canada’s qualifying rate, or whatever your contracted mortgage rate is plus two percent.James Laird is the co-founder of Ratehub and President of CanWise Financial. He’s crunched the numbers and he figures that the stricter stress test rules make housing about 20 percent less affordable. For buyers like DiCarlo, who lives in downtown Toronto and is hoping to buy there, condo prices have appreciated about 10 percent in the past year. With the Bank of Canada raising rates, and economists predicting three more hikes next year… It all adds up. “Many people might actually be in worse shape now than they were a year and a half ago even though they saved a lot of money because these things are running away from them,” he says.The rate hikes alone are worth considering, for anyone examining the changing budgeting scenario. If you take the average home in Canada, priced at $487,000, with a “typical” millennial down payment of 10 percent, amortized over 25 years with a five-year variable rate of 2.45 percent (which is what the scenario was like at the start of 2018), that equals a monthly mortgage payment of $2,013. The three rate increases we’ve seen this year means the homeowner pays an extra $173 in monthly mortgage payments. Each rate increase translates into more than $50 of additional money every month, towards home ownership.

In addition to the five rate hikes (three total this year), condo prices in Toronto continue to outperform and those cater to a lot of millennial buyers. So while prospective buyers like DiCarlo have been saving, prices have risen. He also has to save more to qualify for a mortgage because of new federal rules, known as B20, imposed by Canada’s top bank regulator. As of January 1, home ownership hopefuls like DiCarlo must prove they can service a mortgage based on one of two things (depending on which is higher): the Bank of Canada’s qualifying rate, or whatever your contracted mortgage rate is plus two percent.James Laird is the co-founder of Ratehub and President of CanWise Financial. He’s crunched the numbers and he figures that the stricter stress test rules make housing about 20 percent less affordable. For buyers like DiCarlo, who lives in downtown Toronto and is hoping to buy there, condo prices have appreciated about 10 percent in the past year. With the Bank of Canada raising rates, and economists predicting three more hikes next year… It all adds up. “Many people might actually be in worse shape now than they were a year and a half ago even though they saved a lot of money because these things are running away from them,” he says.The rate hikes alone are worth considering, for anyone examining the changing budgeting scenario. If you take the average home in Canada, priced at $487,000, with a “typical” millennial down payment of 10 percent, amortized over 25 years with a five-year variable rate of 2.45 percent (which is what the scenario was like at the start of 2018), that equals a monthly mortgage payment of $2,013. The three rate increases we’ve seen this year means the homeowner pays an extra $173 in monthly mortgage payments. Each rate increase translates into more than $50 of additional money every month, towards home ownership. Based on what the central bank stated today, there are several more rate hikes in the near future because the economy is doing relatively well and most of the uncertainty surrounding a North American trade deal has been lifted. “The Bank of Canada has strongly indicated that rates will continue to rise, so Canadians shopping for a home who want a fixed rate should get pre-approved as quickly as they can,” suggests Laird.These budgetary calculations should also be taken into consideration for people who already have a fixed mortgage. Their payments are unaffected until they’re up for renewal, but experts say they should prepare for higher monthly mortgage costs.For prospective buyers like DiCarlo, it means setting your sights on something less expensive or waiting longer to get into the housing market. But Tal says waiting comes at a cost too, especially in the city of Toronto. “As you know, the rental market is extremely expensive at this point so in this sense, they lose on both sides. They cannot buy and rent is expensive. That’s a very difficult situation to be in.”Follow Anne on Twitter and Instagram.

Based on what the central bank stated today, there are several more rate hikes in the near future because the economy is doing relatively well and most of the uncertainty surrounding a North American trade deal has been lifted. “The Bank of Canada has strongly indicated that rates will continue to rise, so Canadians shopping for a home who want a fixed rate should get pre-approved as quickly as they can,” suggests Laird.These budgetary calculations should also be taken into consideration for people who already have a fixed mortgage. Their payments are unaffected until they’re up for renewal, but experts say they should prepare for higher monthly mortgage costs.For prospective buyers like DiCarlo, it means setting your sights on something less expensive or waiting longer to get into the housing market. But Tal says waiting comes at a cost too, especially in the city of Toronto. “As you know, the rental market is extremely expensive at this point so in this sense, they lose on both sides. They cannot buy and rent is expensive. That’s a very difficult situation to be in.”Follow Anne on Twitter and Instagram.

Advertisement

Advertisement